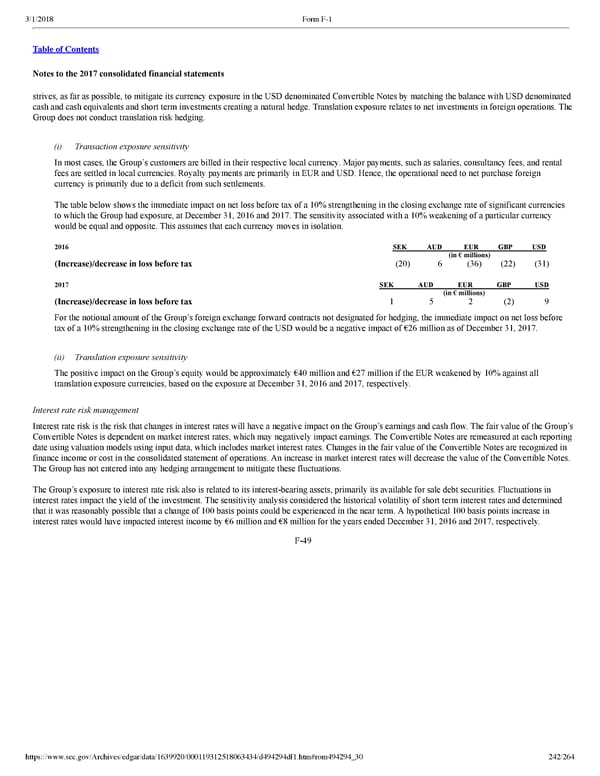

242/264 Notes to the 2017 consolidated financial statements strives, as far as possible, to mitigate its currency exposure in the USD denominated Convertible Notes by matching the balance with USD denominated cash and cash equivalents and short term investments creating a natural hedge. Translation exposure relates to net investments in foreign operations. The Group does not conduct translation risk hedging. (i) Transaction exposure sensitivity In most cases, the Group’s customers are billed in their respective local currency. Major payments, such as salaries, consultancy fees, and rental fees are settled in local currencies. Royalty payments are primarily in EUR and USD. Hence, the operational need to net purchase foreign currency is primarily due to a deficit from such settlements. The table below shows the immediate impact on net loss before tax of a 10% strengthening in the closing exchange rate of significant currencies to which the Group had exposure, at December 31, 2016 and 2017. The sensitivity associated with a 10% weakening of a particular currency would be equal and opposite. This assumes that each currency moves in isolation. 2016 SEK AUD EUR GBP USD (in € millions) (Increase)/decrease in loss before tax (20 ) 6 (36 ) (22 ) (31 ) 2017 SEK AUD EUR GBP USD (in € millions) (Increase)/decrease in loss before tax 1 5 2 (2 ) 9 For the notional amount of the Group’s foreign exchange forward contracts not designated for hedging, the immediate impact on net loss before tax of a 10% strengthening in the closing exchange rate of the USD would be a negative impact of €26 million as of December 31, 2017. (ii) Translation exposure sensitivity The positive impact on the Group’s equity would be approximately €40 million and €27 million if the EUR weakened by 10% against all translation exposure currencies, based on the exposure at December 31, 2016 and 2017, respectively. Interest rate risk management Interest rate risk is the risk that changes in interest rates will have a negative impact on the Group’s earnings and cash flow. The fair value of the Group’s Convertible Notes is dependent on market interest rates, which may negatively impact earnings. The Convertible Notes are remeasured at each reporting date using valuation models using input data, which includes market interest rates. Changes in the fair value of the Convertible Notes are recognized in finance income or cost in the consolidated statement of operations. An increase in market interest rates will decrease the value of the Convertible Notes. The Group has not entered into any hedging arrangement to mitigate these fluctuations. The Group’s exposure to interest rate risk also is related to its interestbearing assets, primarily its available for sale debt securities. Fluctuations in interest rates impact the yield of the investment. The sensitivity analysis considered the historical volatility of short term interest rates and determined that it was reasonably possible that a change of 100 basis points could be experienced in the near term. A hypothetical 100 basis points increase in interest rates would have impacted interest income by €6 million and €8 million for the years ended December 31, 2016 and 2017, respectively. F49

Spotify F1 | Interactive Prospectus Page 241 Page 243

Spotify F1 | Interactive Prospectus Page 241 Page 243